AI Is Winning the Capital Race. Here Is What That Means for Every Founder Who Is Not Building in AI.

- Shawn Jhanji

- May 11

- 4 min read

The numbers are in for Q1 2026, and the headline story is straightforward: UK equity investment is holding steady at roughly £6 billion per quarter, the UK remains Europe's dominant destination for venture capital, and the market is, on the surface, healthy.

But Beauhurst's Deal Q1 2026 report, published this week, tells a more complicated story underneath the headline. Capital is concentrating. Deal volumes are falling. A small number of AI mega-rounds are doing most of the heavy lifting. And the structural question the data raises is one that goes to the heart of how early-stage founders outside AI are experiencing this market right now.

The Concentration Problem

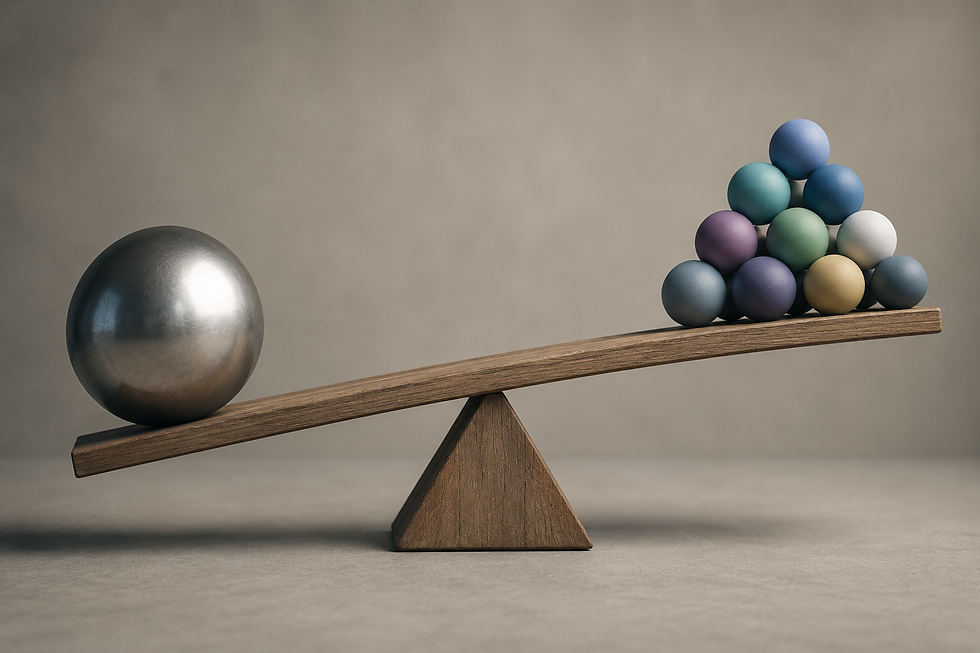

UK equity investment has held steady for five consecutive quarters in headline terms. But the composition of that stability has changed dramatically. In Q1 2026, a handful of mega-rounds in the AI and infrastructure space accounted for nearly half of all equity raised in the UK. Rounds including NScale ($2 billion), Wayve ($1.2 billion) and ElevenLabs ($500 million) are structurally distorting the aggregate picture. Hosting, robotics and transportation were the most funded sectors, driven by a small number of very large AI-led deals.

Meanwhile, deal volumes continue to fall. Fewer companies are completing equity rounds than at any point since 2021. The rounds that do happen are getting larger, but the pool of companies accessing them is narrowing. Capital is concentrating into AI, into conviction bets, into a smaller number of winners.

What This Means for Non-AI Founders

This is where the Beauhurst data gets quietly significant. The structural story of Q1 2026 is not just about AI winning. It is about what happens to the cohort of founders in healthtech, fintech, deeptech, and climate who raised in previous years and are now approaching the market for follow-on capital.

These founders are entering a market in which investors with finite fund capacity are being asked to double down on AI portfolio companies while simultaneously fielding follow-on requests from companies built on fundamentally different theses. The arithmetic is tight. Funds that deployed across multiple sectors in 2021 and 2022 now carry AI positions that are appreciating in ways that require capital to support, while non-AI portfolio companies are reaching inflection points that require follow-on support too.

The crowding-out risk is real. It does not manifest as explicit bias or rejection — it manifests as stretched attention, deferred decisions, and a structural preference for the thesis that is already winning. For a healthtech founder with strong clinical data but no AI narrative, the question of whether their investor still has capacity and conviction for the next round is not abstract. It is the central question of their next twelve months.

The Data Behind the Pattern

Beauhurst's data shows deal volumes at their lowest since 2021. The UK has not lost its position in European venture — it still raises more than France, Germany and the Netherlands combined. But the distribution of that capital has narrowed significantly. What looks like market health at the aggregate level is, at the company level, a market that is increasingly winner-take-most.

This matters for the structural question at the centre of this publication: who gets funded, and why. If the answer is increasingly AI companies with large rounds, then the question becomes what mechanisms exist for founders outside that category to access capital efficiently. The traditional VC route, already difficult for founders outside London, outside established networks, and outside the currently preferred investment thesis, is getting more difficult still.

Where This Leads

The Beauhurst data is not a counsel of despair. The UK's AI leadership is genuine — it creates more AI startups and unicorns than any other European country, generates four times the enterprise value of its nearest European peers. These are real outcomes. But the ecosystem question is whether the infrastructure for capital formation is flexible enough to serve founders who are building real, commercially significant businesses in sectors that are not currently attracting mega-rounds.

That is a question about efficiency and reach. It is also a question that better capital formation infrastructure — including the emerging tokenisation layer that is beginning to make private equity more portable and more accessible to a wider range of qualified investors — is beginning to answer. Not fully, not yet. But the direction of travel is meaningful.

Key Takeaways

Beauhurst's Deal Q1 2026 report shows UK equity holding steady at around £6 billion per quarter, but deal volumes at their lowest since 2021.

A small number of AI mega-rounds are accounting for nearly half of all equity raised, distorting the aggregate picture.

Non-AI founders approaching the market for follow-on capital face structural crowding-out risk from funds with stretched capacity.

Capital is concentrating into fewer, larger, higher-conviction rounds — a pattern that has accelerated through 2025 and into 2026.

The structural question for the wider ecosystem is whether capital formation infrastructure is flexible enough to serve commercially significant founders outside the AI narrative.

Sources: Beauhurst newsletter “The Deal Q1 2026,” received 8 May 2026. https://www.beauhurst.com/research/ | Disruption Banking Q1 2026 analysis: https://www.disruptionbanking.com/2026/04/15/uk-vc-investment-gathers-pace-in-q1-2026-as-ai-and-megarounds-drive-late-stage-surge/

Comments