Euroclear and Societe Generale Test Stablecoin Settlement for Tokenised Commercial Paper

- Shawn Jhanji

- Jul 1

- 3 min read

Settlement is the least glamorous word in finance and quite possibly the most important. It is the moment a trade actually completes, when cash and asset change hands and the deal becomes real. For decades that moment has taken days, propped up by a chain of intermediaries each taking a cut and adding a delay. So when one of the institutions that sits at the centre of that machine starts testing a faster way to do it, founders and investors watching the tokenisation story should pay attention, even if the instrument involved sounds obscure.

On 25 June, Euroclear, one of the world's largest settlement houses, and SG-FORGE, the digital assets arm of Societe Generale, said they would explore using a regulated stablecoin to settle tokenised short term debt. The test will use USD CoinVertible, SG-FORGE's MiCA compliant US dollar stablecoin, to settle tokenised, dollar denominated Negotiable European Commercial Paper. Euroclear will act as the core settlement infrastructure for the pilot.

What is actually being tested

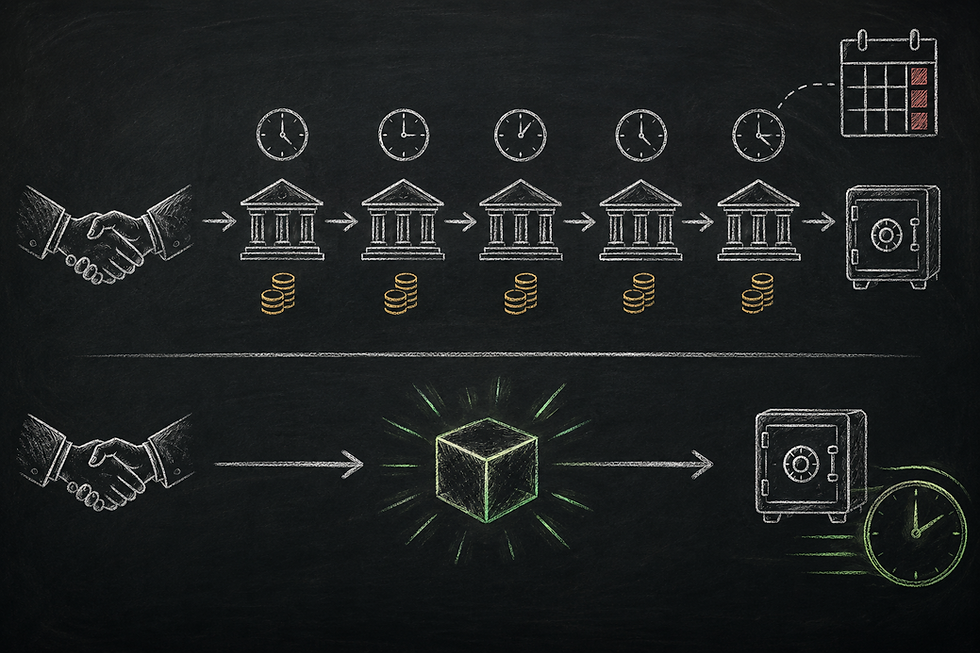

Strip away the jargon and the idea is simple. Commercial paper is short term IOU style debt that companies issue to raise cash quickly. Today, a European issuer wanting dollar funding through this market navigates a slow, multi step settlement process. The pilot puts the debt itself on a digital ledger as a token, and puts the cash leg on the ledger too, in the form of a regulated dollar stablecoin. When the two are matched, settlement can happen close to instantly, with the payment and the asset moving together rather than chasing each other across separate systems.

The attraction for issuers is practical. Dollar funding is often cheaper or deeper than euro funding, and a digital cash settlement model makes reaching dollar investors faster and less operationally heavy. The pilot sits alongside Project Pythagore, a parallel effort to move euro denominated commercial paper onto distributed ledger technology with settlement in central bank money.

Why it matters beyond the back office

The headline names are wholesale institutions and the instrument is one most founders will never touch. The significance is in the pattern. The hardest part of tokenisation was never minting a token to represent an asset. It was building settlement plumbing that regulated institutions trust enough to run real money through. Each pilot like this one normalises the idea that a regulated stablecoin is acceptable settlement cash, and that a tokenised security can settle against it within an established market infrastructure rather than an experimental sandbox.

That foundation is the same one private and startup equity will eventually run on. The rails being laid for tokenised commercial paper, with atomic settlement and regulated digital cash, are the rails that make tokenised shares, secondary liquidity and faster capital formation realistic later. It is also notable that SG-FORGE is using a MiCA compliant stablecoin, anchoring the experiment inside Europe's regulatory perimeter rather than outside it, which is precisely what gives conservative institutions the confidence to take part.

For the UK, the read across is clear. As the FCA and Bank of England work through their Digital Securities Sandbox and their joint vision for tokenised wholesale markets, the question of what counts as acceptable settlement cash, and how tokenised assets settle against it, is moving from theory to live testing on the continent. The infrastructure decisions being made now will shape how quickly tokenised equity becomes a practical option for British companies.

Key takeaways

Euroclear and SG-FORGE will test settling tokenised, dollar denominated commercial paper using USD CoinVertible, a MiCA compliant dollar stablecoin, with Euroclear as the settlement infrastructure.

The pilot puts both the debt and the cash on a ledger, enabling near instant settlement where payment and asset move together.

The real significance is institutional trust in settlement plumbing, the hardest and most decisive part of tokenisation, not the tokens themselves.

The same rails being proven for tokenised debt are the foundation that tokenised equity and private market liquidity will eventually depend on.

Sources: Ledger Insights; Asset Servicing Times; Global Custodian; PostTrade360.

Comments